RMB交易与研究

Anopaquegroupofalgorithmicmoneymanagershaveseizedcontroloftheoilmarket.

一群不透明的算法基金经理已经控制了石油市场。

Tradingoilhasperhapsneverbeenmoreofarollercoasterridethanitistoday.石油贸易也许从来没有像今天这样像坐过山车一样。

Justinthepasttwomonths,pricesthreatenedtoreach$100perbarrel,onlytowhipsawintothe$70s.OnonedayinOctober,theyswungasmuchas6%.Andsofarin2023,futureshavelurchedbymorethan$2aday161times,amassivejumpfrompreviousyears.就在过去两个月,油价曾一度升至每桶100美元,但随后又飙升至每桶70美元。10月的一天,它们的波动幅度高达6%。2023年迄今为止,期货价格每天上涨超过2美元的次数已达161次,较往年大幅上涨。

What’shappeningcan’tbeentirelyexplainedbyOPEC’smachinations,orwarintheMiddleEast.Whilesupply-and-demandfundamentalsstilldictateoverallcommoditypricecycles,theday-to-daybusinessoftradingcrudefuturesisincreasinglydominatedbyspeculativeforces,fuelingvolatilityanddrivingadisconnectbetweenphysicalandpapermarkets.所发生的事情不能完全用欧佩克的阴谋或中东战争来解释。尽管供需基本面仍然决定着整体大宗商品价格周期,但原油期货交易的日常业务日益受到投机力量的主导,加剧了波动性并导致实物市场和纸质市场之间的脱节。

Andit‘snotjustspeculatorsingeneral—tradersarepointingthefingeratanopaquegroupofalgorithmicmoneymanagersknownascommoditytradingadvisors.不仅仅是投机者——交易员还把矛头指向了一群不透明的算法资金管理者,即商品交易顾问。

Despitetheirmundanename,CTAshaveemergedasapowerfulforceintheoilmarket.Thoughtheycomprisejustone-fifthofmanagedmoneyparticipantsinUSoil,CTAsmadeupnearly60%ofthegroup’snettradingvolumethisyearbysomemeasures,accordingtoBridgetonResearchGroup,whichprovidesanalyticsoncomputer-generatedtrades.That’sthebiggestsharethegrouphasheldindatagoingbackto2017.尽管名字很平常,但CTA已成为石油市场上的一股强大力量。根据提供计算机生成交易分析的布里奇顿研究集团(BridgetonResearchGroup)的数据,尽管CTA仅占美国石油管理资金参与者的五分之一,但从某些指标来看,今年CTA占该集团净交易量的近60%。这是该集团自2017年以来在数据中所占的最大份额。

Whileit’shardtoquantifyhowmuchoftotaltradingvolumesarecontrolledbyCTAs,algosmorebroadlyareresponsibleforasmuchas70%ofcrudetradesonanaverageday,accordingtodatafromTDBankandJPMorgan.根据道明银行(TDBank)和摩根大通(JPMorgan)的数据,虽然很难量化CTA控制了总交易量的多少,但更广泛地说,算法平均每天占原油交易的70%。

“Youwouldbeabsolutelyshockedhowlargetheirpositionsare,”said IliaBouchouev,aformertraderandmanagingpartneratPentathlonInvestmentswhoteachesatNewYorkUniversity.“TheyareprobablybiggerthanBP,ShellandKochcombined.”“你会对他们的头寸有多大感到震惊,”在纽约大学任教的PentathlonInvestments前交易员兼管理合伙人IliaBouchouev说。“它们可能比英国石油公司、壳牌和科氏公司的总和还要大。

Thisyear’svolatilepriceswingsarebeingintensifiedbythesebots,accordingtointerviewswithmorethanadozentraders,analystsandmoneymanagerswhoworkintheoilmarket.They’veroiledcommoditiesfromgasolinetogold,sidelinedtraditionalinvestors,drawntheireofOPECandevenraisedeyebrowsattheWhiteHouse.根据对十几位在石油市场工作的交易员、分析师和基金经理的采访,这些机器人正在加剧今年波动的价格波动。他们扰乱了从汽油到黄金的大宗商品,使传统投资者边缘化,引起了欧佩克的愤怒,甚至在白宫引起了人们的注意。

CTAsarelooselylabeledasanindividualororganizationthatadvisesonthetradingoffutures,optionsorswaps.Butthoseintheknowsaymostaredefinedbytheirtradingstrategies:computer-drivenandrules-based,withrelativelylimitedtimehorizons.CTA被松散地标记为就期货、期权或掉期交易提供建议的个人或组织。但知情人士表示,大多数交易策略都是由他们的交易策略决定的:计算机驱动和基于规则,时间范围相对有限。

WhatmakesalgorithmicCTAssodestabilizingisthatthey’retypicallytrendfollowers—andtrendexaggerators.Whenpricesgodown,theysell,drivingthemevenlower.And,moretroublingforconsumers,thesameistrueontheupside.算法CTA之所以如此不稳定,是因为它们通常是趋势的追随者——也是趋势的夸大者。当价格下跌时,它们会卖出,从而进一步压低价格。而且,对消费者来说更令人不安的是,从好的方面来看也是如此。

SomeanalystssayCTAscontributedtoovervaluingoilbyasmuchas$7abarrelduringarecentrally.AndWhiteHouseofficialsbelievetheyplayedasignificantroleinpricerun-upsduringthecourseof2023,accordingtoapersonfamiliarwiththematter.一些分析师表示,在最近的一次反弹中,CTA导致油价高估了每桶7美元。据一位知情人士透露,白宫官员认为,他们在2023年的价格上涨中发挥了重要作用。

Even$1or$2addedtothepriceofabarrelfiltersdowntoconsumersthroughhigherfuelcostsatatimewhenenergy-driveninflationisamongthebiggestobstaclesfortheworld’scentralbankers.InAugust,forexample,higherpricesmeantthatgasolinecostsaccountedforhalfoftheincreaseintheUSconsumerpriceindex.在能源驱动的通货膨胀是世界央行行长面临的最大障碍之一的时候,即使是每桶价格增加1美元或2美元,也会通过更高的燃料成本过滤到消费者身上。例如,8月份,价格上涨意味着汽油成本占美国消费者价格指数涨幅的一半。

“TheFederalReserveshouldbeawareofthemandtheirinfluenceinmarkets,”said RebeccaBabin,aseniorenergytraderforCIBCPrivateWealthinNewYork.“美联储应该意识到它们及其对市场的影响力,”CIBCPrivateWealth驻纽约的高级能源交易员RebeccaBabin表示。

“CTAscancreatethesefractures—periodsoftimewhenwe’retradingawayfromfundamentals,”Babinsaid.Andwhilethosemomentsmaybeshort-lived,theensuingpriceswings“readthroughintothebroadereconomicworldinalotofdifferentways,”shesaid.“CTA可能会造成这些裂缝-我们远离基本面的时期,”巴宾说。她说,虽然这些时刻可能是短暂的,但随之而来的价格波动“以许多不同的方式渗透到更广泛的经济世界中”。

BigSwings,BigProfit动,大利润

WhilealgorithmicCTAsaddmuch-neededliquiditytothemarket,theirtradingstrategiescanamplifydailyswingstoanextreme.In2022,whenCTAtradingvolumesrapidlyexpanded,NewYorkoilfuturespostedamore-than$2dailymove242times.That’s150%higherthanthehistoricalaveragesince2000,accordingtoBloombergcalculations.虽然算法CTA为市场增加了急需的流动性,但它们的交易策略可能会将每日波动放大到极端。2022年,当CTA交易量迅速扩大时,纽约石油期货的日涨幅超过2美元,上涨了242次。彭博社计算,这比2000年以来的历史平均水平高出150%。

Butwhat’ssosurprisingaboutthecontinuedvolatilityin2023isthatit’scomewithoutthemajorshocktosuppliesthatfollowedRussia’sinvasionofUkraine.WhileIsrael’sconflictwithHamassetmarketsonedge,it’snotyethadanymajorimpactonoilflows.AndralliesbuoyedbyproductioncutsfromtheOrganizationofPetroleumExportingCountriesanditsallieshavebeenundercutbyCTAactivity.但令人惊讶的是,2023年的持续波动并没有像俄罗斯入侵乌克兰后那样对供应造成重大冲击。虽然以色列与哈马斯的冲突使市场处于紧张状态,但它尚未对石油流动产生任何重大影响。石油输出国组织(OrganizationofPetroleumExportingCountries)及其盟国减产提振的反弹也被CTA活动所削弱。

Theunpredictabilityofthisyear’smarketswingshaven’tbeenkindtohumantraders,manyofwhomaremakinglessmoneyonoilthantheydidlastyearwhentheyrakedinrecordgains,accordingtomarketparticipants.据市场参与者称,今年市场波动的不可预测性对人类交易员来说并不友好,他们中的许多人在石油上赚的钱比去年创纪录时少。

CTAs,bycontrast,havebeenbooming—notchingthreestraightyearsofgainsinenergymarkets,accordingtoStephenRosemeofBridgeton.相比之下,CTA一直在蓬勃发展——根据布里奇顿的斯蒂芬·罗斯姆(StephenRoseme)的说法,能源市场连续三年上涨。

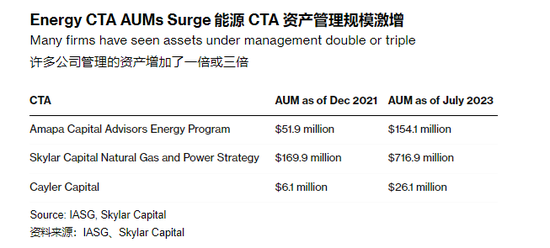

AndmanyCTAsareexpanding.Paris-basedCapitalFundManagementsaysitsCTA’sassetsundermanagementjumpedto$3.8billioninJuly2023from$2.4billioninDecember2021.AmapaCapitalAdvisorsLLCandSkylarCapitalManagementareamongCTAsthathavedoubledortripledassetsundermanagementinlessthantwoyears,CTAadvisoryfirmIASGreports.ThelargestCTAsinenergyareManAHL,Gresham,LynxandAlphaSimplex,accordingtoBarclayHedge,buttheirexactvolumesaredifficulttoquantify.许多CTA正在扩大。总部位于巴黎的资本基金管理公司表示,其CTA管理的资产从2021年12月的24亿美元跃升至2023年7月的38亿美元。据CTA咨询公司IASG报道,AmapaCapitalAdvisorsLLC和SkylarCapitalManagement是CTA之一,在不到两年的时间里,管理的资产增加了一倍或三倍。根据BarclayHedge的数据,能源领域最大的CTA是ManAHL,Gresham,Lynx和AlphaSimplex,但它们的确切数量很难量化。

ManVersusMachine人与机器

ThebeautyofalgorithmicCTAs,accordingtothehumansbehindthem,isthatthey’reuntaintedbybiasandimpulse—they’repredominatelymathematical.Thatapproach,ofcourse,isanathematomanyincommodities,whereman’sdominionovernature,andmarkets,isfoundational.根据算法CTA背后的人的说法,算法CTA的美妙之处在于它们不受偏见和冲动的影响——它们主要是数学的。当然,这种方法对许多大宗商品来说是诅咒的,因为在大宗商品中,人类对自然和市场的统治是基础。

“Everytraderthinksthey’rethebest.Everytraderthinkstheyhavetheedge,”saysBrentBelote,whogaveupanoiltradingcareeratthebiggestUSbank, JPMorganChase&Co,tolaunchhisownCTAin2016.“每个交易者都认为自己是最好的。每个交易员都认为他们有优势,“布伦特·贝洛特说,他放弃了美国最大的银行摩根大通的石油交易生涯,于2016年推出了自己的CTA。

Trustingamachinedidn’tcomenaturallytoBelote.Althoughhe’sbuiltsixalgos,heinitiallyfoundhimselftradingalongsidethem.Afterall,hehadyearsofexpertisethatthecomputerdidnot.贝洛特并不自然而然地相信机器。尽管他已经构建了六种算法,但他最初发现自己是在与它们一起进行交易。毕竟,他拥有计算机所没有的多年专业知识。

WhenRussiainvadedUkraineinearly2022andBrentcrudefuturesskyrocketed35%totradeabove$120abarrel,Belotewanteddesperatelytodirecthisalgos.ItwasasubzeromorninginJackson,Wyoming,whenherosetocheckonhismodels–buthedecidednottointervene.Intheaftermathoftheinvasion,hisfirm, CaylerCapital,returned25%toinvestors,hesaid.Thatcompareswith1%forBloomberg’shedgefundindex.当俄罗斯于2022年初入侵乌克兰、布伦特原油期货价格飙升35%至每桶120美元以上时,贝洛特迫切希望指导他的算法。那是怀俄明州杰克逊的一个零下的早晨,他起身去检查他的模型,但他决定不干预。他说,入侵之后,他的公司凯勒资本(CaylerCapital)向投资者返还了25%。相比之下,彭博对冲基金指数为1%。

“Thenumbersdon’tlie,”saidBelote.

“数字不会说谎,”贝洛特说。

Not‘FlashBoys’不是“闪光男孩”

CTAsthemselvesaren’tnew—they’vebeenaroundsincetheearlydaysoffuturestrading.Andsince1984,they’vehadtoregisterwiththeNationalFuturesAssociation.Theytypicallyenjoyalowerbarriertoentrythanhedgefunds,whichcantradeawidervarietyofsecuritiesandrequiremoreinitialcapital.CTA本身并不新鲜——它们从期货交易的早期就已经存在了。自1984年以来,他们必须在全国期货协会注册。与对冲基金相比,它们的进入门槛通常较低,对冲基金可以交易更广泛的证券,并且需要更多的初始资本。

They’renotreallythe“FlashBoys”offutures,though.CTAs,unlikehigh-frequencytraders,aren’ttypicallyprofitingfromthespeedatwhichtheymove.Instead,theymostlymakemoneyonindicatorsfueledbytrends.Andthey’reactiveinequitiesandcommoditiesalikethroughfuturesandoptions.不过,他们并不是真正的未来“闪光男孩”。与高频交易者不同,商品交易顾问通常不会从交易速度中获利。相反,他们主要通过趋势推动的指标赚钱。他们通过期货和期权活跃于股票和大宗商品领域。

Marketsforcommodities,however,differfromequitiesinmanyimportantrespects.Forexample,whilethestockmarketevolvedasawaytoraisecapital,commoditiesfuturesmarketshavetraditionallybeenaplaceforproducersandbuyerstohedgetheirpricerisk.然而,大宗商品市场在许多重要方面与股票市场不同。例如,虽然股票市场是作为筹集资金的一种方式而发展的,但商品期货市场传统上一直是生产商和买家对冲价格风险的场所。

BornFromtheCrash从崩溃中诞生

HowdidCTAscometobecomesodominant?Likemanycurrentphenomena,theanswerstartsinthedepthsofthepandemic.CTA为何变得如此占主导地位?与当前许多现象一样,答案始于大流行的深层原因。

Asshutdownsengulfedtheworldin2020,fuelconsumptioncollapsedbymorethanaquarter.Allhellbrokelooseinthecrudemarket.ThebenchmarkUSoilpricebrieflydroppedtominus$40abarrelandinvestorswereinwhollynewterritory.Somefundsthattooklonger-termviewsbasedonsupply-and-demandfundamentalsquicklypulledout.2020年,随着全球范围内停工,燃料消耗下降了四分之一以上。原油市场彻底崩溃了。美国基准油价短暂跌至每桶负40美元,投资者进入了全新的领域。一些基于供需基本面采取长期观点的基金迅速撤离。

Suchbearmarketsprovedtobe“extinctionevents”fortraditionalfunds,whichmadeway“foralgosupremacy,”thebulkofwhichareCTAs,said DanielGhali,seniorcommoditystrategistatTDSecurities.Russia’sinvasionofUkrainegavetheCTAsanotherfoothold.Spikingvolatilityinthefuturesmarketdrovemanyremainingtraditionalinvestorstotheexits,andopeninterestinthemainoilcontractstumbledtoasix-yearlow.道明证券(TDSecurities)高级大宗商品策略师丹尼尔·加利(DanielGhali)表示,这种熊市被证明是传统基金的“灭绝事件”,为“算法霸权”让路,其中大部分是CTA。俄罗斯对乌克兰的入侵为CTA提供了另一个立足点。期货市场的剧烈波动迫使许多剩余的传统投资者退出,主要石油合约的未平仓合约跌至六年低点。

Thatcoincidedwiththecollapseofanothersourceoffuturesandoptionstrading:oil-productionhedging.Duringtheheydayofshaleexpansionaboutadecadeago,drillerswouldlockinfuturespricestohelpfundtheirgrowth.Butintheaftermathofthepandemic-inducedpricecrash,achastenedUSoilindustryincreasinglyfocusedonreturningcashtoinvestorsandeschewedhedging,whichcanoftenlimitacompany‘sexposuretotheupsideinarisingmarket.Bythefirstquarterofthisyear,thevolumeofoilthatUSproducerswerehedgingbyusingderivativescontractshadfallenbymorethantwo-thirdscomparedwithbeforethepandemic,accordingtoBloombergNEFdata.与此同时,期货和期权交易的另一个来源:石油生产对冲也崩溃了。大约十年前,在页岩气扩张的鼎盛时期,钻探商会锁定期货价格,为其增长提供资金。但在大流行引发的价格暴跌之后,受到打击的美国石油行业越来越注重向投资者返还现金,并回避对冲,这往往会限制公司在上涨的市场中的上行风险。彭博新能源财经的数据显示,到今年第一季度,美国生产商利用衍生品合约进行对冲的石油量比疫情爆发前下降了三分之二以上。

TherecentwaveofdealmakingbyUSoilproducersthreatenstofurtheracceleratethedeclineinhedging.Andit’shighlylikelythatCTAswillcontinuetofillthevacuumleftbythosetraditionalmarketplayers.美国石油生产商最近的交易浪潮有可能进一步加速对冲的下滑。CTA很可能会继续填补这些传统市场参与者留下的真空。

Insomeways,theriseoftheCTAsisjuststarting.That’sevidenttoBouchouevofNYU,whosaysthathisstudentsconsiderworkingatthefundsa“dreamjob.”从某些方面来说,CTA的崛起才刚刚开始。对于纽约大学的布霍耶夫来说,这一点显而易见,他说他的学生认为在该基金工作是一项“梦想的工作”。

“CTAsareanexampleofhowtechnologyisgettingintoourspace,”hesaid.“You’dbeadinosaurafterawhileifyourejectit.”“CTA是技术如何进入我们领域的一个例子,”他说。“如果你拒绝它,过一段时间你就会变成恐龙。”

(原文来源于BBG网络版,以英语专业学习为目的)

本文链接地址是https://www.qihuo88.net/qhzx/30234.html,转载请注明来源